05 Feb Fixed or Variable

Fixed or Variable

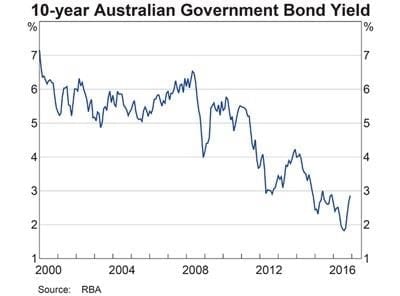

It’s been headline news for some time, Australian bond markets have been sold off in recent months increasing the yield (interest rates) at the back end of the yield curve (3 – 10 years). This means the swap curve where banks benchmark their fixed rate pricing has gone up as well.

Below is a snap shot of where our 10-year government bonds are trading (circa 2.80%) from a low of circa 1.82% in August 2016. That is a full 1.00% increase in 5 months. Wow!

aking into consideration that Economics is the only field in which two people can share a Nobel Prize for saying the opposite thing, there is plenty of heated argument as to why the yields are going up, it’s continuation to go up, or it bouncing off 3.00% and begin to fall again.

This paper is not about direction, but about motivation.

To Fix or Float

There are 4 main drivers that can decipher your decision-making process. Let’s go through each one briefly.

- The Gambler: Too often consideration is taken on speculating that interest rates are going to continue to go up or down. An emotional response to this is acting on sentiment rather than economic rationality. If motivation to hedge interest rates on your thoughts that interest rates have bottomed and are on the way up for good, then rethink your philosophy on hedging. Your motivations, albeit with good intentions, may not be aligned with your business requirements (refer to point d). Look at 2008 when bonds hit 4.00%. A reaction (and most likely when bond rates bounced to 4.5%) that gamblers predicted the bottom and locked in, missing the next 2.80% fall in rates.

- The Fearful: Fear of missing the bottom of the cycle and the fear of interest rates going up. Fear is a very powerful motivation and it is difficult to separate this emotional response to economic reality. After all it is a primal instinct for self-preservation. Smell your fear, then lock it in a sealed box.

- The Risk Taker: On the flip side, borrowers may let it all run on the premise that rates may fall further even though their business may be extremely sensitive to interest rate movements and gross margin profit (or loss). The risk taker can take a skewed position on markets that may not be all too favourable when rates move against the play. Save your risk play over a game of 500, it is much safer.

- The Rational Centurion: This is where a borrower needs to be. Completely independent from the emotional drivers and strapped into the decision-making chair of economic rationale. Here decisions are made on the following questions been logically answered;

- What are my future capital requirements and movements over the next 3 – 5 years (the period where hedging takes place). Is there a need to hedge when debt reduction is planned?

- What percentage of this capital requires flexibility to ensure capital mobility can be deployed without incurring substantial break fees?

- What is the real sensitivity of my business to interest rates? Can the predicted cash flow handle an increase in rates (with regards to the banking covenants and policy ratios)?

- What premium in interest rates am I willing to pay on day one with a hedge to remove a percentage of this? Calculate the economics (refer to my example below).

- Does my business have a natural hedge to interest rates (ie assets that appreciate with inflation and / or increased profits are expected in an economy that is picking up speed).

The Economics of Hedging:

This is best played out with an example.

On a $5,000,000 borrowing, the following rates are provided to a borrower;

Variable rate : 4.25%

(benchmarked against 90 day BBSY)

3 year fixed rate: 5 .25%

5 year fixed rate : 5.85%

If the borrower decides to hedge $1.5m for 3 years and $1.5m for 5 years, the borrower is paying a weighted average premium of 1.30% for $3,000,000 from day 1 over the first 3 years

In simple terms that is around 5 RBA rate rises before the hedge breaks even. But remember the business has paid a premium leading to this point. Therefore, the rates must continue rising 5 more times (now 10 in total) over the same amount of time it took to hit break even before the business breaks even in the premium paid.

Obviously multiple scenarios can be modelled out quite easily, but it demonstrates that the economics run deeper when applied to probability over a specific time frame. Noting that in the end, the hedge will expire at some point and the business is back to the variable environment. So, whatever the interest rates are at this point of maturity, can the business handle high interest rates at all?

It then comes back to the first 4 points under 4). The Rational Centurion.

This is a heavy topic, and we hope this blog has triggered some deeper thought. We are most willing to discuss these points in more detail with you if it strikes some curiosity and relevance to your business.

Sorry, the comment form is closed at this time.